Does the Bond Market Have it All Wrong?

Over at one of my faves, the Big Picture Blog, Barry Ritholtz asks: Does the Bond Market Have it All Wrong?.

Implicit in this discussion: "Dose the Federal Reserve have it all wrong?"

Of course nobody knows the answer yet, but we don't have to travel very far to find an example of when both were very wrong:

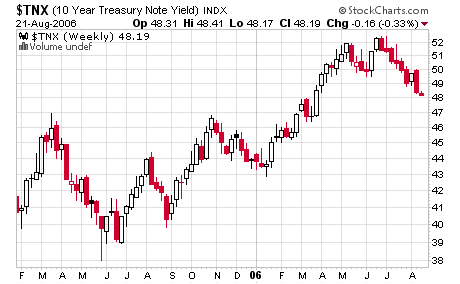

That's a chart of the yield on the Ten Year US Treasury. Not only do you see a dramatic spike from 3.80 to 5 1/4% (about a 40% jump in rates), but what you don't see is the previous dip to the neighborhood of 3% back in 2003.

Three years ago the Fed was warning of DE-flation and reassuring the markets that they had plenty of tools available to avoid Japan's policy mistakes (what some have called Japan's economic depression).

A year ago certain members of the Fed were confidently predicting oil and other commodities would decline, and that inflation was well under control.

Keep in mind as you look at that chart the dollar value of the treasury bond market is absolutely enormous. Thus, relatively small changes in yield translate into very large gains/losses. In addition, there are countless loans and other instruments pegged to various yields along the curve.

In other words, a whole lot more at stake than just what it costs the government to get a loan.

Thus, the more cerebral types (think: Bill Gross) inhabit the bond market trenches, and as an extension, the bond market get it's reputation for being the more reliable leading indicator.

The truth is the bond market can be every bit as volatile as the stock market, and some would argue the Fed's crystal ball has been in the shop for quite a long time now.

I have been fond of saying that the equity traders are the hormonal teenagers of the capital markets (traders think of markets as a daily version of Hot or Not?).

In our metaphor, the Bond market is the so-called adult supervision. Bond vigilantes have long been thought of as applying much needed pressure to the Feds to keep inflation under control, and rein in the deficit spending habits of the Federal government.

Implicit in this discussion: "Dose the Federal Reserve have it all wrong?"

Of course nobody knows the answer yet, but we don't have to travel very far to find an example of when both were very wrong:

That's a chart of the yield on the Ten Year US Treasury. Not only do you see a dramatic spike from 3.80 to 5 1/4% (about a 40% jump in rates), but what you don't see is the previous dip to the neighborhood of 3% back in 2003.

Three years ago the Fed was warning of DE-flation and reassuring the markets that they had plenty of tools available to avoid Japan's policy mistakes (what some have called Japan's economic depression).

A year ago certain members of the Fed were confidently predicting oil and other commodities would decline, and that inflation was well under control.

Keep in mind as you look at that chart the dollar value of the treasury bond market is absolutely enormous. Thus, relatively small changes in yield translate into very large gains/losses. In addition, there are countless loans and other instruments pegged to various yields along the curve.

In other words, a whole lot more at stake than just what it costs the government to get a loan.

Thus, the more cerebral types (think: Bill Gross) inhabit the bond market trenches, and as an extension, the bond market get it's reputation for being the more reliable leading indicator.

The truth is the bond market can be every bit as volatile as the stock market, and some would argue the Fed's crystal ball has been in the shop for quite a long time now.

posted by FRx at 2:27 PM

![]()

![]()

subscribe

subscribe

0 Comments:

Post a Comment

<< Home